Share

Overview

After a dismal start to 2024—with the measurement of EV readiness falling dramatically in the big 5 markets during the first quarter—there were signs of recovery during Q2 in all of those markets with the exception of France. However, in the vehicle market-place sales have slowed, and the share of electric cars during the first six months of the year has lagged noticeably behind the levels achieved in 2023.

Consumer interest remains worryingly low, and it is this factor that is currently most suppressing demand for EVs. Digital interest, as measured by traffic to EV model pages on car brand websites, actually fell in all of the markets that we monitor apart from in the UK and Norway.

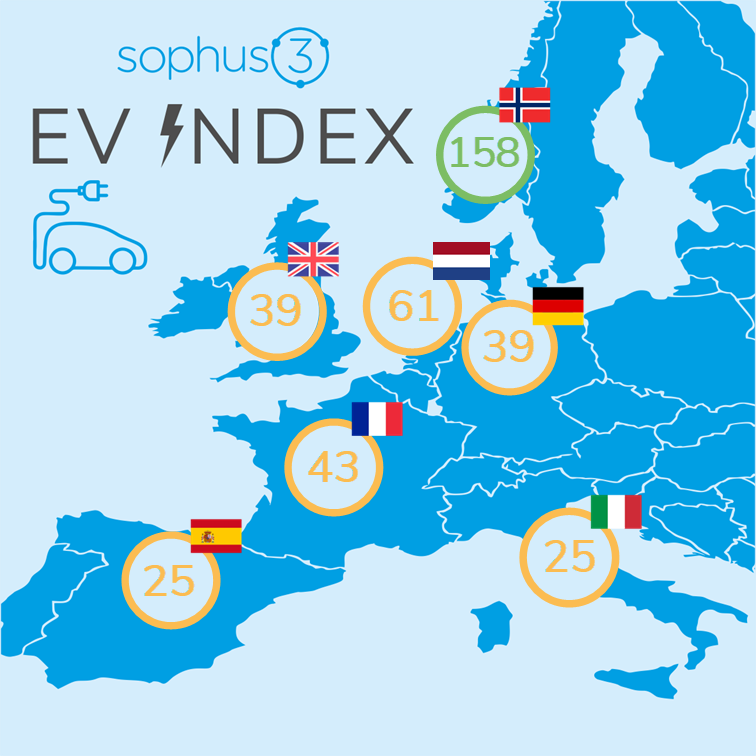

EV Index 2024 Q2

Figures in brackets show change from 2024 Q1

| EV Index | Consumer Interest | Affordability & Choice | Infrastructure | |

| Germany |

41 (2) |

25 (0) | 58 (9) |

63 (5) |

| Spain |

27 (2) |

14 (0) | 49 (11) |

57 (-1) |

| France |

42 (-1) |

24 (-4) | 55 (10) |

86 (2) |

| Italy |

26 (1) |

14 (0) | 44 (7) |

55 (1) |

| UK |

42 (3) |

29 (1) | 55 (12) |

55 (-3) |

| Netherlands |

68 (7) |

45 (3) | 57 (8) | 218 (13) |

|

Norway |

121 (–) |

326 (–) | 93 (–) |

91 (–) |

(The Netherlands and Norway provide benchmarks for comparison as ‘best in class’ performers in their efforts to encourage EV adoption.)

Affordability

Unusually the biggest area of improvement in the three ‘pillars’ from which the overall index is calculated, was in the pricing/affordability of EVs relative to their fossil-fuelled equivalents. It is important to understand that this shift is not due to the sudden appearance of a rash of budget-priced offerings in the new vehicle market. Rather, it is the result of some changes in the sales ranking of the models that we track so that some of the more expensive EVs— for example the BMW iX and Jaguar I-Pace—have been dropped from the calculations. In addition, as the market has slowed, manufacturers have looked at increasing their discounts on different models. Again, the shifts are not that dramatic. Whilst there is some variation between local markets and different brands, across all of the markets that we track, EV prices have fallen by an average of only 1%, whilst ICE prices have increased by barely 3%.

Tariffs on Chinese EVs

Particularly in the near term, hopes of a significant reduction in the premium that an electric car buyer is forced to pay look to be receding. At the beginning of July the European Commission imposed provisional tariffs that could be as high as 48% on imported Chinese EVs having ruled that the Chinese government’s subsidy of its home industry was damaging to EU’s carmakers.

From a consumer’s point of view this effectively delays the availability of affordable EV options and therefore the main result will be to slow the transition to zero emission vehicles.

How effective these measures will be in achieving the objective of protecting the region’s car industry is also debatable. Many commentators think it unlikely that they will blunt the Chinese OEMs’ charge into Europe and that instead a tit-for-tat response from the government in Beijing will cause more serious damage to the European brands that are heavily reliant on the Chinese market. The view is that manufacturing groups like BYD and SAIC enjoy sufficient margin to be able to absorb these tariffs, whilst many brands—including BYD, MG, Chery and most recently Zeekr—are planning to open manufacturing facilities within Europe which would exempt them from these measures in the not too distant future.

Norway and the UK are pursuing a different path from the European Union in refusing, for the present, to implement tariffs against the Chinese brands so it will be interesting to see how pricing, and EV uptake, evolves in those markets over the coming months.

BYD is one of a number of Chinese brands planning to build cars in Europe, in its case at Szeged, Hungary.

Infrastructure

The index shows that public charging facilities continue to keep pace with the expansion of the electric fleet and are not the impediment to EV acquisition that many insist. Whilst there would clearly be bottlenecks and frustrations for EV drivers if adoption of the powertrain were to suddenly accelerate, the present rate of public charger provision is adequate in the majority of markets. The UK for example is reported to be adding a public charge point to the network every 25 minutes; in Germany, the most recent emphasis is on the roll out of a rapid charger network to support heavy duty trucks, with 350 locations earmarked for development from the end of the summer.

Political shifts

The recent period has been marked by a number of changes in the political landscape in Europe which have raised uncertainties about regional and national policies encouraging the transition to EVs and broader carbon reduction measures.

The European elections produced a shift to the right which threatened the bloc’s future commitment to the 2035 timetable for the phase out of ICE vehicles. The re-appointment of Ursula von der Leyen as European Commission President ensures that, for the moment, a consensus supporting this policy remains in place despite a growing number of dissenting voices.

The recent UK election, that saw a Labour landslide, seems unlikely to produce any immediate rollback in EV policy. The French elections resulted in advances by both a left coalition and the far right creating a stalemate that threatens progress on sustainability issues.

In Italy the nationalist government, despite introducing a subsidy scheme to encourage purchase of greener cars, continues to argue against the timetable for the transition to EVs. It has also been at odds with Stellantis over its embrace of electrification and the group’s choice of manufacturing sites.

Summary: slow progress to a point of crisis

The European Union and U.K. share the objective of ending sales of fossil-fuelled cars by 2035. Stepped targets are in place with manufacturers facing large penalties if they fail to meet them. In the UK, EVs must make up 22% of overall sales this year, increasing to 25% next year. (Within the European Union the steps are similar but defined by the carbon dioxide emissions of the vehicle fleet.)

European sales figures for EVs in the first half of the year show that progress has been extremely modest with just a 1.3% increase over the same period last year. Electric cars currently account for only 12.5% of the EU new car market, a lower share than the 14.4% achieved at the end of 2024, although the UK is further forward with EVs enjoying 16.6% market share year-to-date.

But the trajectory in both markets suggests that those targets are going to be missed by a wide margin. A crisis point has been reached which can no longer be ignored and it seems inevitable that tensions between car makers and governments will come to a head in the near future.

About

The EV Index from Sophus3 provides an objective measure of the readiness of the vehicle market to enable and encourage the mainstream adoption of electric vehicles (EVs).

The index is formed from three pillars, each measuring distinct factors that help or hinder electric vehicle acquisition. First of these is the consumer appetite to buy electric, the second is the capability of the automotive companies to supply these cars, and the third is the availability of suitable charging infrastructure.

A score of 100 represents parity in the attractiveness, availability, pricing and usability of an electric car compared with a conventionally fuelled vehicle.

We publish the EV Index for the UK, Germany, France, Italy, Spain, The Netherlands, and Norway.

A fuller explanation of the EV Index from Sophus3 can be found here.

If you would like to discuss this latest issue of the EV Index please contact: patrick.fuller@sophus3.com